By John Hawkins

Suddenly the talk in global financial markets has spun from “When will interest rates next rise?” to “How soon before they fall?”.

Some commentators are flagging the shift as a “pivot party”.

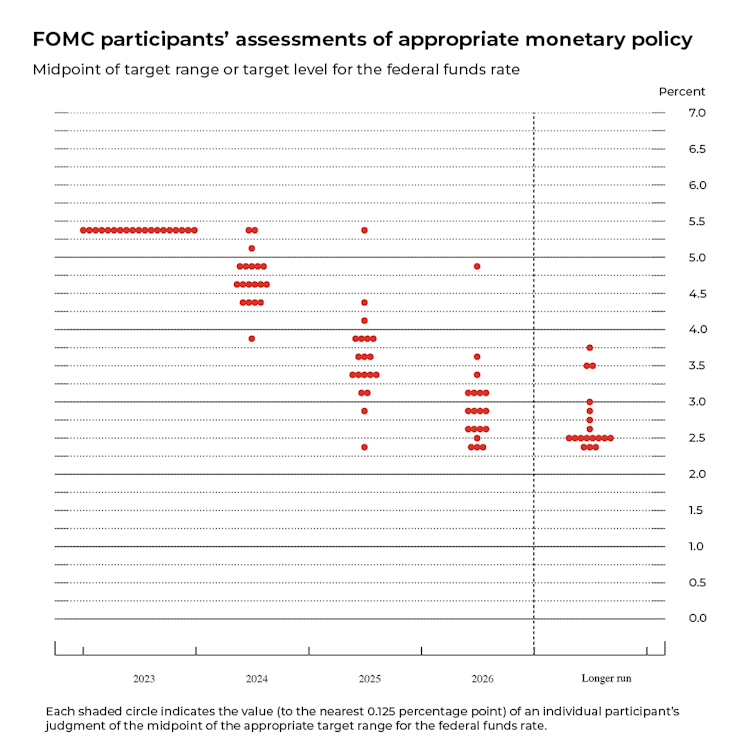

This change has been most prominent in the United States. It was prompted by the Federal Reserve, the US equivalent of the Reserve Bank of Australia, releasing its latest “dot chart”. This shows most members of its policy-setting Federal Open Market Committee expect their interest rate would be lower by the end of 2024.

The recent review of the Reserve Bank in Australia wanted more transparency. But, after the whacking former Governor Phil Lowe got when he wrongly predicted rates would stay low until “at least” 2024, I doubt his successor Michele Bullock will be keen to publish a similar chart.

Even so, financial markets in Australia are also now implying interest rates will fall over the course of next year.

The latest indicators

The Australian economy has continued to slow according to the latest national accounts. Consumer spending did not increase at all in the September quarter, despite an increase in population. Exports contracted. Overall GDP grew by a mere 0.2%.

The news from the labour market was mixed. There was a solid rise in employment in November. The hours worked data, however, have been flat for the past six months.

The government maintained fiscal discipline in the mid-year budget update released last week. They saved rather than spent almost all the extra revenue from higher-than-expected commodity prices.

The minutes of the Reserve’s latest meeting on December 5 show the board noted “encouraging signs of progress” in returning inflation to the target.

Subsequent events have suggested inflation will likely continue on its downward trajectory, which means the Reserve has increased interest rates enough.

Another development since the Reserve last met is an update of the Statement on the Conduct of Monetary Policy between Treasurer Jim Chalmers and the board. This sets out the common understanding between them about Australia’s monetary policy framework.

Much of this statement carries over the existing framework. The bank’s primary tool is its cash rate target and it is varied to achieve a medium-term inflation target of 2-3%. Employment considerations influence how quickly it is regained when shocks move inflation away from it.

The statement explicitly refers to the midpoint of the target, reflecting a suggestion in the recent Reserve Bank review. Some commentators have interpreted this as indicating the bank cannot cut rates as its forecast for inflation only has it reaching the top, not the middle, of the range by the end of 2025.

I disagree. The bank has always aimed at the midpoint of the target as the most likely way to ensure inflation averages within it. If the board was happy at its December meeting to have reached 3% by the end of 2025 on its way to achieving 2.5% later, there is no reason for it to change this view in February.

So what will the Reserve Bank do?

On balance, the economic news does not suggest the Reserve Bank will feel a need to raise rates in February. But with inflation still high, and plenty of uncertainty, they are unlikely to cut rates any time soon. The bank does not generally make sharp U-turns with the average gap between the last interest rate increase in a cycle and the first cut being ten months.

At its next meeting, on February 5-6, the Reserve board may have a new member, Deputy Governor Andrew Hauser, and a new adviser, Chief Economist Sarah Hunter. They share a British background so will be familiar with the Bank of England model, which influenced the Reserve Bank review.

The impact of (eventual) lower interest rates

The movements in the Reserve Bank’s interest rate matter most to the third of households with a mortgage. Most of these have variable-rate loans where the interest rate closely follows that set by the Reserve. An interest rate cut would ease the cost-of-living pressures they have been facing.

A household with an average loan size of around A$600,000 would have seen their monthly repayments rise by almost $1,700 since early 2022. This would drop by $100 if rates were cut by 0.25%.

While the impact on mortgagees always gets the most attention, interest rates affect other members of the community too.

Lower interest rates mean a lower income to retirees dependent on interest on their savings. They tend to boost the prices of assets such as shares and houses. They encourage borrowing and spending and reduce incentives to save. They tend to lower the exchange rate, making imports more expensive for Australians but our exports cheaper to foreigners. The net impact is generally to lower unemployment.

A lot of people are therefore looking forward to an interest rate cut. But they should not be holding their breath.

Financial markets may be getting prematurely excited. The last thing the Reserve Bank would want is to find themselves having lowered rates too quickly and see inflation turn back up, necessitating the interest rate cut to be reversed. More likely, they will wait for inflation to drop much closer to their target before there is any easing of interest rates.

John Hawkins, Senior Lecturer, Canberra School of Politics, Economics and Society, University of Canberra

This article is republished from The Conversation under a Creative Commons license. Read the original article.

Support Our Journalism

Global Indian Diaspora needs fair, non-hyphenated, and questioning journalism, packed with on-ground reporting. The Australia Today – with exceptional reporters, columnists, and editors – is doing just that. Sustaining this needs support from wonderful readers like you.

Whether you live in Australia, the United Kingdom, Canada, the United States of America, or India you can take a paid subscription by clicking Patreon. Buy an annual ‘The Australia Today Membership’ to support independent journalism and get special benefits.