")

By Natalie Peng

You want your superannuation savings to be invested in things that also serve the planet’s long-term interests. But how can you be sure your fund’s values align with yours – or even its own claims?

This question has become increasingly pertinent as demand for environmentally and socially sustainable investments grows – and with it incentives for financial institutions to put the best spin on their offerings.

One consultancy specialising in “responsible investment” reckons 10% of the funds it has examined do not have the sustainability orientation they claim.

Among those accused of greenwashing in recent months is one of Australia’s biggest super funds, HESTA (the industry fund for health and community service workers), which has promoting its “clean energy” credentials while still holding shares in fossil-fuel companies Woodside and Santos.

So how can you check what your superannuation fund invests in?

Super funds are legally obliged to disclose how they invest your money in two different disclosure documents – a Product Disclosure Statement and a Portfolio Holdings Disclosure.

Both will be available on a super fund’s website, though how easily you can find them will vary.

The rest of this article is going to explain what information these documents provide, how useful this information is likely to be, and your best bet to ensure your super fund reflects your values.

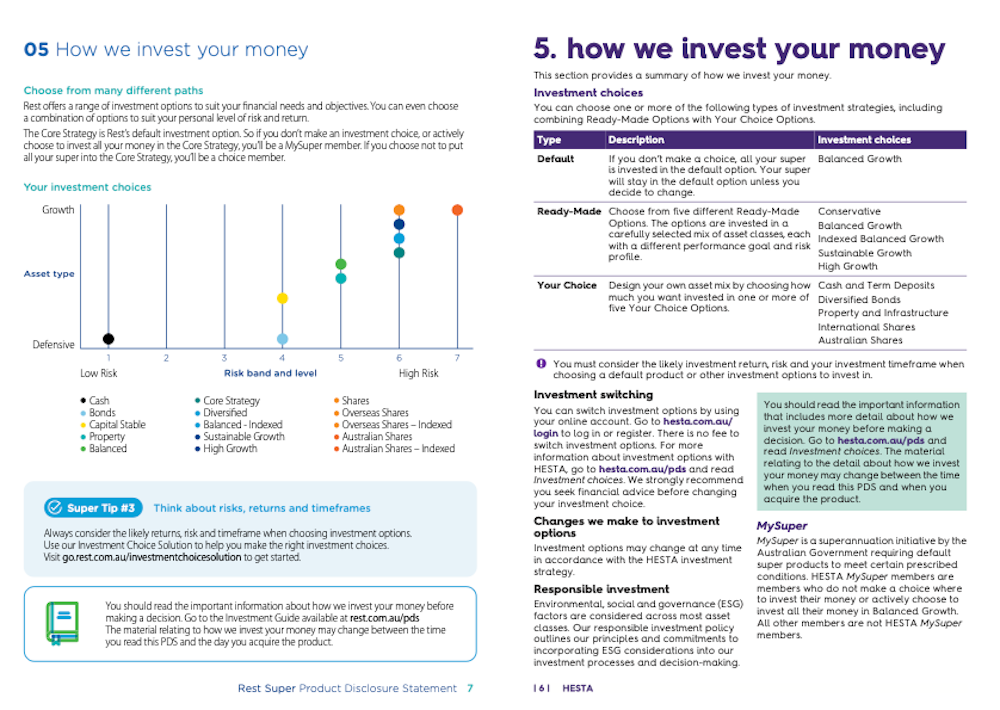

The Product Disclosure Statement

Product disclosure statements are required by the financial regulator (the Australian Securities and Investments Commission) for all financial products.

This document outlines the most basic but important information of an investment product’s features, benefits, risks and costs, including fees and taxes. The format is standardised, with one section (Section 5) covering with “How we invest your money”.

The information it contains is broad. At best you’ll learn how the fund splits its investments between safe and riskier assets, and between different asset classes – Australian shares, international shares, property trusts, infrastructure trust, cash and so on.

Portfolio Holding Disclosure

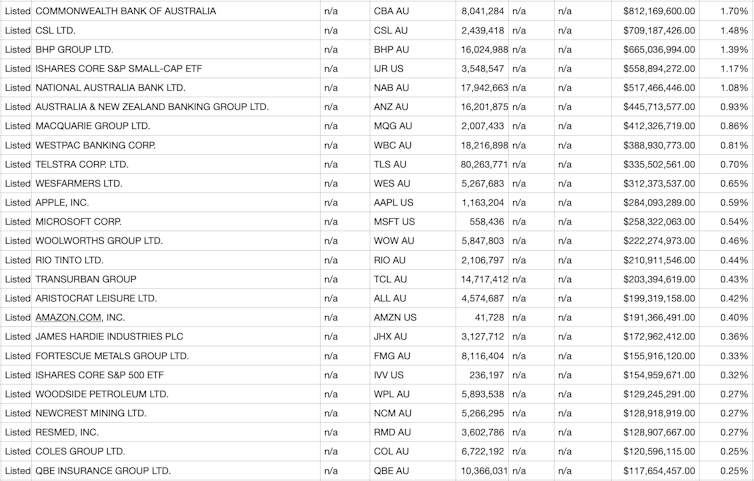

For a comprehensive look at where your money is invested in, you can consider the Portfolio Holdings Disclosure.

This document lists a fund’s complete holdings – including the percentage and value of every single company stock held.

Portfolio holdings disclosures are relatively new, being obligatory only since March 2022 under legislation meant to improve transparency in the sector.

However, super funds aren’t obliged to provide this information in a consistent, easily understandable way.

For a non-expert who doesn’t know what to look for, the level of detail can be mind-boggling. You may find yourself scrutinising a spreadsheet listing thousands of items.

The Australian Retirement Trust’s Portfolio Holdings Disclosure for its “Lifecycle Balanced Pool”, for example, has more than 8,000 line items.

Some super funds have made the effort to provide this information in a more user-friendly format. An example is Future Super, which allows you to search and filter portfolio holdings by asset class and country of origin.

But if your concern is to avoid investing in some specific activity such as in mining fossil fuels or gambling, you’ll need to know the companies and other assets you want to avoid for this to be helpful.

Your best options

This is not to say portfolio holding disclosure obligations are useless. They are incredibly useful – a huge leap forward in the sector’s accountability. They just aren’t designed for consumers.

So there is still much work to be done to make the sector truly transparent.

What would really help is independent certification and ratings of super products, similar to government websites and programs that certify energy efficiency and allow comparison of electricity plans.

In the meantime, I can offer you one big tip.

Choose a specific superannuation product that markets itself on its environmental or social sustainability credentials. Most super funds now provide these choices alongside their more traditional investment options.

There is a variety of “screening” approaches to ethical investments. Some exclude entire sectors. Others include the best environmental and social performers even among “sinful” industries such as tobacco or weapons.

So just because a super product is marketed as “ethical” or “sustainable” doesn’t guarantee you will agree with all its investments.

But there is a much higher likelihood of it living up to its claims due to greater scrutiny by third parties such as environmental groups as well as the financial regulator.

The Australian Securities and Investments Commission put super funds on notice earlier this year with a “guidance note” about the growing risk of greenwashing in sustainability-related financial products.

It reminded funds that “making statements (or disseminating information) that are false or misleading, or engaging in dishonest, misleading or deceptive conduct in relation to a financial product or financial service” is against the law.

So super funds know their portfolios are being scrutinised.

Switching your investment option or fund is simpler than you think. You only need to fill out and lodge a form. Just be sure to compare fees and performance, and seek a second opinion from trustworthy adviser before “voting with your wallet”.

Natalie Peng, Lecturer in Accounting, The University of Queensland

This article is republished from The Conversation under a Creative Commons license. Read the original article.